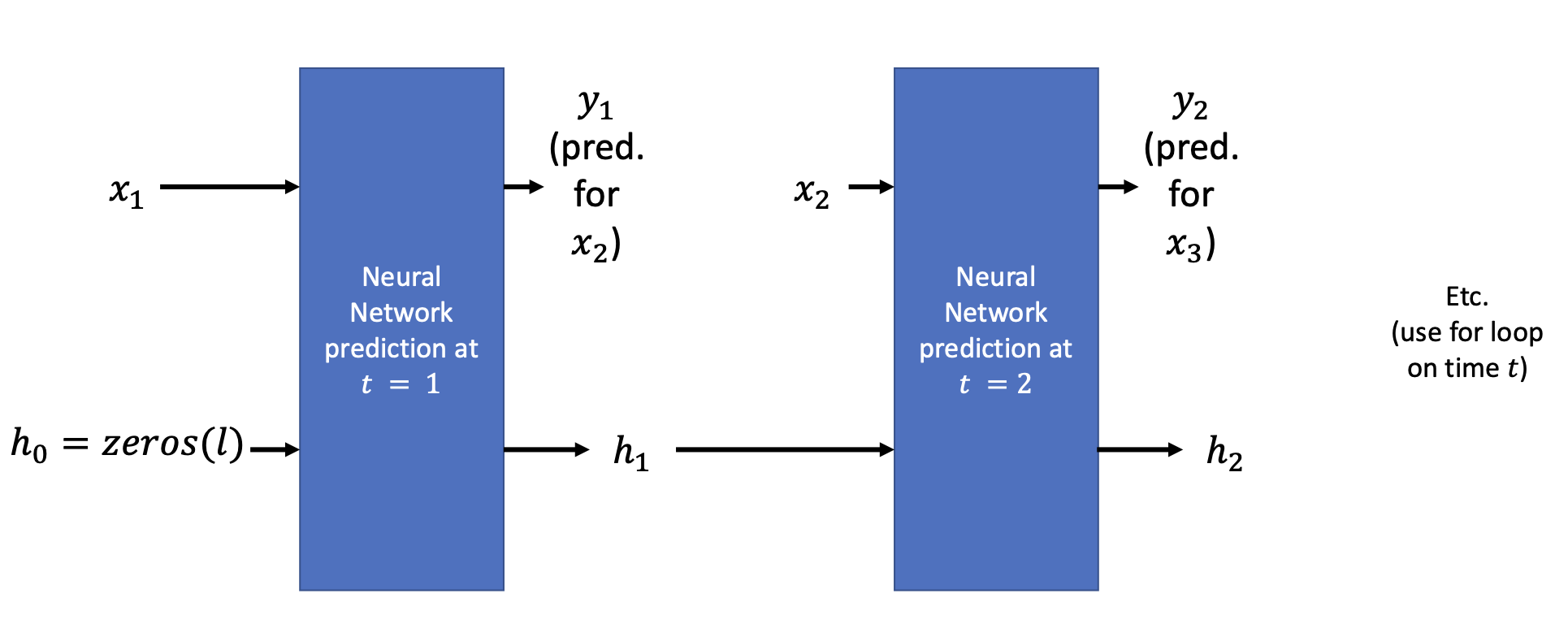

Recurrent Neural Networks

Neural Networks that receive inputs of observation

at time and memory vector as outputs at time , to compute a prediction for and updated memory vector

Memory lookback

Lookback or window size refers to the number of past observations/values of a time series that is used to make a prediction

Consider the time scale of the problem to decide on appropriate lookback length:

- Daily stock price prediction: Lookback length

of 30 days - Hourly traffic patterns: Lookback length

of 24 hours

Typically, look at the seasonality and trend (see Time series dataset#Decomposition)

Backpropagation through time

Batches of

- Unfolding RNN operations over time

- Run predictions on

consecutive samples and keep track of loss - Perform one parameter update after

samples

Vanishing gradient problem

We encounter the Vanishing gradients problem:

- Each hidden state

is updated via a function of previous states and input - During training, backpropagation through time can result in very small gradients for earlier time steps, where the weights are then updated

- This is problematic as RNNs are designed to handle time series data, which can exhibit long-term dependencies

- This is even more problematic if the RNN uses activation functions that saturate such as Sigmoid function or tanh function due to repeated multiplication of small derivatives and weights

- As a result, weights associated with long-term dependencies update very slowly or not at all

- The solution is to use specialised architectures such as Long Short-Term Memory and Gated Recurrent Units

Long Short-Term Memory and Gated Recurrent Units models work by creating more sophisticated RNN units with internal mechanisms (gates) to control the flow of information and regulate the state updates, explicitly managing what to remember and what to forget.

This decouples the task of prediction (

LSTMs vs GRUs

| LSTMs > GRUs | LSTMs < GRUs |

|---|---|

| Designed to maintain and propagate info over longer time lags than GRUs, hence better suited for tasks that require network to retain info for longer periods | Fewer parameters, hence faster to train and less prone to overfitting; more computationally efficient |

| More parameters, hence more expressive and better able to model complex nonlinear functions | Have a simpler structure than LSTMs, hence easier to implement and understand |

| Can handle input sequences of variable lengths more effectively, given they have an explicit memory cell to store info over multiple timesteps | More effective in handling sequences with a lot of noise or missing data as they are able to adapt to changes |

| Better suited for prioritisiation of recently observed due to the gating mechanism |

Autoregressive RNNs

A type of RNN (often used in decoders) where the prediction

from the current time step is used as the input for the next time step

In autoregressive RNNs, the model generates sequences by feeding its own outputs back as inputs.

The encoder reads an input sequence (e.g., a French sentence, a user's question) and produces a context vector (Se).

Then, the decoder:

- Uses

Seas its initial hidden stateand a special "start-of-sequence" token as the first input e.g. <s> - Predicts the first output word

- Uses

as the next input to predict the second output word - Continues step 3 until a special "end-of-sequence" token e.g.

</s>token is generated or maximum length is reached

Autoregressive models can be harder to train because errors can accumulate. If a model makes a bad prediction early on, the incorrect prediction that is fed back in can lead to future errors - exposure bias.